Strong global polyethylene film production fuelled by food

packaging innovations and emerging markets

The brand-new report from AMI Consulting - Polyethylene Film – The Global Market 2021 maps the worldwide landscape of production and trade flows in the polyethylene (PE) film industry, together with providing critical insight on resin usage and demand trends in key consumer and industrial applications.

Common technology platforms and the commoditisation of polyethylene grades means the film extrusion market is becoming increasingly global. Together with changing patterns of demand, the PE film industry is entering a new era, with more mature Western markets, China’s push towards greater self-sufficiency and resin supply migrating to faster growing markets such as India, or to areas with a feedstock advantage i.e. North America and the Middle East.

Asia and Australasia remains the largest production hub for PE film, with China the single largest manufacturing nation. From a demand perspective, it is developing markets, fuelled by young and growing populations, urbanisation and emerging middle classes, which offer the most growth potential. Meanwhile, in mature Western markets, growth rates are lower and producers are more focused on customised technical innovation to increase the range of end-use applications. Sustainability and environmental concerns are also shaping production trends and influencing material innovation in all regions, including MDO-PE and BOPE for monomaterial, “recycle-ready” packaging.

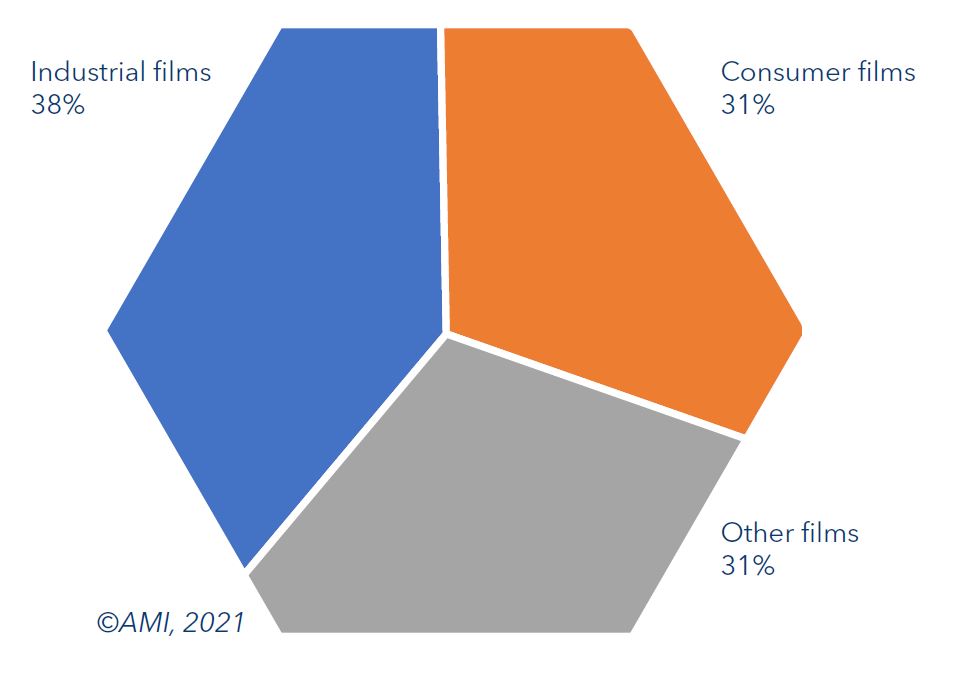

Global polyethylene films production by type 2020

The progression of end-use applications varies, influenced by socio-economic factors and regional market maturity. Prior to the Covid-19 pandemic, healthcare and hygiene films were already enjoying robust growth, albeit from a low base, to cater to the needs of aging populations and improving medical provisions in emerging markets. The onset of the pandemic brought soaring additional demand for personal protective equipment (PPE). In response, many companies pivoted their operations into areas of high demand, such as medical aprons and other disposables.

Food packaging accounts for the largest production volume globally, with growth continuing to be spurred by changing consumer lifestyles which require more convenience products. This category has also benefitted from increased demand during the pandemic, with consumers appreciative of its safety and hygiene benefits. In contrast, the production of PE film for retail carrier bags is declining as a result of taxes and bans on the production and/or distribution of single-use lightweight plastic (primarily HDPE) retail bags in countries around the world. As a consequence, HDPE’s share of overall polymer use is declining.

Companies active in the industry in addition to those considering entering the market for the first time, must understand the trends that determine aspects including future industry size and structure. In this competitive market, knowledge is critical to the development of successful strategies for growth in sales and profitability.

The 2021 edition of AMI’s Polyethylene Films – The Global Market Report provides a detailed independent assessment of the industry which is becoming increasingly global in scope. Key issues addressed in the study include production and demand drivers in each of six global regions, in addition to a detailed review of global imports and exports data. Film and bag production is also analysed by end-use application and raw material type, with a forecast to 2025.

This comprehensive study builds on and expands AMI’s successful reports and databases related to the PE film industry and enables industry players to:

- Get unrivalled data on the size and structure of the global industry

- Identify key material trends for consumer and industrial films

- Assess growth dynamics

- Determine supply economics by region

- Understand the evolution of trade flows and impact on supply

- Evaluate the future outlook for global PE film production and trade

For further information, please contact:

Charmaine Russell,

Consumer and Industrial Films Unit Manager, AMI Consulting